While most 20-somethings are busy scrolling through social media, somehow convincing themselves that avocado toast is a reasonable daily breakfast expense, you are likely here because you want more. Perhaps you are wondering if you should be doing something different with your money, or if you’re destined to join the ranks of people who complain about being broke while simultaneously ordering DoorDash three times a week.

Here is something that might shock you: The purchases you make in your 20s will determine whether you spend your 30s building serious wealth or still living paycheck to paycheck, trapped in some sort of financial groundhog day.

Most people get this completely backwards. They think their 20s are exclusively for spending money on “experiences” and “stuff,” and that their 30s are for getting serious about money. That is like saying you will start training for a marathon the day before the race. Having spent years analyzing why some people escape the financial hamster wheel while others run on it their entire lives, I have realized that true financial independence is not about luck; it is about strategic consumption.

Living in California, I have seen firsthand how easy it is to fall into the trap of looking rich while being incredibly stressed about paying the bills. The key is to shift your focus from purchases that depreciate to purchases that appreciate or accelerate your earning potential.

Let me be crystal clear: I am not a financial adviser, and this is not financial advice. These are lessons I have learned from watching people succeed and fail with money, including my own experiences of making both incredibly smart moves and spectacularly dumb ones.

What follows are the seven specific purchases that consistently show up in the lives of people who achieve financial independence while they are still young enough to enjoy it.

The Compound Interest Advantage of Your 20s

Before we dive into the specific purchases, we must address the psychological hurdle. Why do your 20s matter so much? The answer is compound interest. The reality is that small, smart decisions made now create massive results down the road.

A hundred dollars invested wisely at age 25 becomes thousands at 50. A hundred dollars spent on something that depreciates becomes nothing but a faded memory, and maybe some stubborn debt. You have an advantage right now that you will never have again: time.

1. Upfront Investment in a Side Hustle

The first purchase that can change your life might surprise you, because it is not something you buy once and forget about. It is an investment in a side hustle.

I know what you are thinking: “A side hustle is a way to make money, not a purchase.” But hear me out, because this is where most people get it wrong. They think side hustles are free. However, the most successful ones require some upfront financial investment to get started properly.

Whether it is buying professional camera equipment for photography, investing in a website domain and hosting for a digital service, purchasing tools for a service-based business, or even just buying books and specialized courses to learn a high-income skill, starting a side hustle almost always requires putting some money down first.

In your 20s, this might be the single best investment you can make. It has the potential to completely change your financial trajectory faster than almost anything else. It diversifies your income and removes your reliance on a single employer.

The beautiful thing about starting side hustles in your 20s is that you likely do not have a mortgage, kids, or a heavy burden of financial obligations weighing you down. You can take risks and try things that might not work out. If you fail, you can bounce back quickly. But if you succeed, you might never have to worry about money again.

The point is not to chase whatever seems most profitable online this week. The point is to find something that matches your existing strengths and interests, then invest what it takes to do it properly.

2. Automating Index Funds Through Tax-Advantaged Accounts

The second purchase that can fundamentally change your life is investing in low-cost index funds, specifically through a Roth IRA or a similar tax-advantaged retirement account.

This is where the magic of compound interest really shows its power. And in your 20s, you have the ultimate unfair advantage: Time.

Let’s look at some math that will blow your mind. If you invest just $200 per month into an S&P 500 index fund starting at age 22, and that investment grows at the historical average of about 10% annually, you will have over $1 million by the time you are 67. Think about that: $200 a month—less than $7 a day—creates millionaire status.

Here is the kicker, and why you cannot wait: If you wait until you are 32 to start that exact same investment plan, you will end up with about $700,000 instead of a million. Waiting 10 years cost you $300,000 in the long run.

The beauty of index funds is that they are basically the boring, reliable friend of the investment world. They don’t promise to make you rich overnight, and they won’t give you exciting stories to tell at parties, but they consistently outperform most actively managed funds over the long term. They spread your risk across hundreds or thousands of companies instead of betting everything on individual stocks.

By using a Roth IRA, your gains grow completely tax-free. Every dollar of growth you earn stays in your pocket when you retire, instead of going to Uncle Sam. It is like having a financial backup plan that runs quietly in the background while you focus on other things. The key is to automate these contributions so the money gets invested before you even see it in your checking account.

3. A Plane Ticket to Travel While You’re Young (But Travel Strategically)

Purchase number three is something that might seem frivolous, but can actually be one of the smartest investments you make. Buy a plane ticket. Travel while you’re young, but the right way—strategically.

This isn’t about blowing your entire savings on expensive vacations to look cool on social media. This is about investing in experiences and connections that can change your perspective and open doors you didn’t even know existed.

Traveling in your 20s builds confidence in ways that nothing else can. When you figure out how to navigate a foreign city, communicate despite language barriers, and solve problems in unfamiliar environments, you develop a kind of self-reliance that serves you for life. You also meet people from different backgrounds and industries who might become valuable connections down the road.

The smart way to do this is by maximizing credit card points and rewards programs. Get a travel rewards credit card, use it for your normal expenses, and pay it off in full every single month. Never carry a balance, but collect those points and use them for free or heavily discounted travel. This strategy also helps you build a strong credit score, which becomes incredibly valuable when you are ready to buy a house or invest in real estate.

4. Education, Workshops, and Skills (Not Just a Degree)

The fourth life-changing purchase is education, but not the kind that puts you $100,000 in debt. I’m talking about books, online courses, workshops, and any other learning that increases your skills and value in the marketplace.

This is honestly one of the most powerful investments you can make, because the knowledge you gain compounds for decades. A $20 book can change your entire mindset about money and success. A few hundred dollars spent on a legitimate course can teach you skills that increase your income by thousands.

The key word here is legitimate. Avoid those $997 courses from people posing next to rented Lamborghinis. Instead, focus on learning from people who have actually built successful businesses or careers in areas you are interested in.

Your brain is most adaptable in your 20s, which means you can learn new skills faster than you will ever be able to again. Take advantage of that. Whether it’s learning to code, understanding digital marketing, developing sales skills, or mastering a trade, every skill you acquire becomes part of your arsenal for the rest of your life.

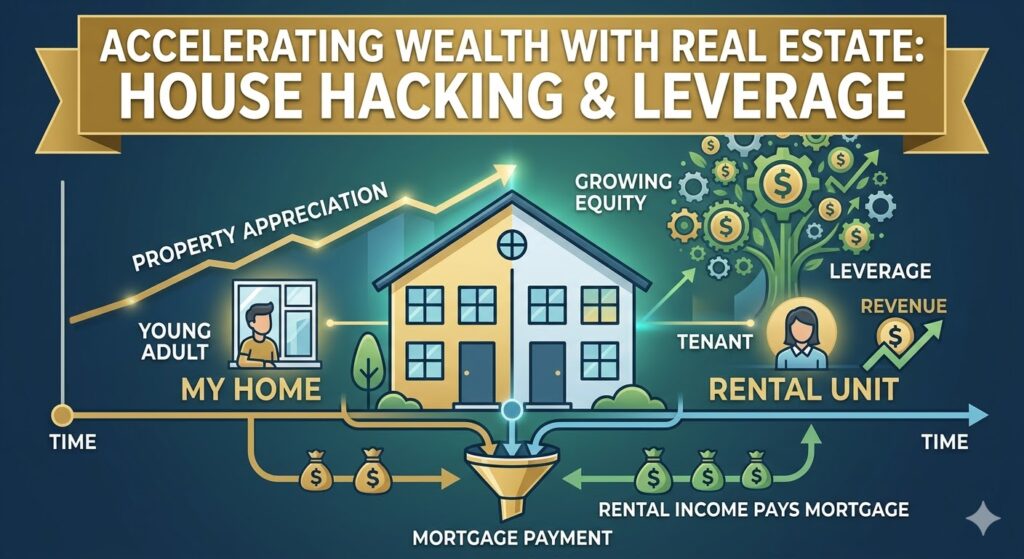

5. Entering the Real Estate Market (House Hacking)

Purchase number five is the big one that scares most people in their 20s, but can absolutely transform your financial future. Buy real estate.

I know what you are thinking: “I can barely afford ramen noodles, let alone a house.” But hear me out, because there are creative ways to make this work, even if you are not rolling in cash. Real estate accelerates wealth building through three main mechanisms:

First, properties generally appreciate in value over time. Second, if you rent part of the property out, you get income that can help pay the mortgage. Third, you are using leverage, meaning you control a valuable asset with a relatively small down payment, and other people are essentially paying for your investment through rents.

If affordability is an issue, consider house hacking. Buy a duplex and live in one unit while renting out the other, or buy a single-family home and rent out rooms to roommates. The goal is to let other people pay your mortgage while you build equity and benefit from appreciation.

It is not always easy, and it definitely requires more hands-on management than index fund investing, but the wealth-building potential is enormous.

6. Cheap, Reliable Transportation

The sixth purchase might sound boring, but it is actually one of the most important financial decisions you will make in your 20s. Buy cheap, reliable transportation.

Notice I did not say buy a car. I said buy transportation. There is a massive difference, and understanding this difference could save you literally hundreds of thousands of dollars over your lifetime.

Most people in their 20s think they need a nice car to look successful. They finance $30,000 vehicles they cannot afford, making payments that eat up a huge chunk of their income for 6 or seven years. Meanwhile, that same money could be growing in investments, compounding into serious wealth by the time they are 40.

Here is the brutal truth about cars: They are not investments. They are depreciating liabilities that cost you money every single month. The moment you drive a new car off the lot, it loses thousands of dollars in value. It is like lighting money on fire, except less fun, and you still have to make payments.

Instead, buy a 3 to 5-year-old Honda Civic, Toyota Corolla, or something similarly reliable for $10 to $15,000. Pay cash if you can or finance it for the shortest term possible. These cars will run for 200,000 miles if you maintain them properly, and they are cheap to insure and repair.

The money you save by not having a car payment can be invested instead. Let’s say you avoid a $500 monthly car payment and invest that money at 8% returns. After 30 years, you will have over $600,000. That is the real cost of having a car payment in your 20s. Plus, when you are not stressed about making car payments, you have more freedom to take risks with your career.

7. The Performance Enhancer: Investments in Your Health

The seventh and final purchase that can change your life is investing in your health. This one gets overlooked constantly, because the benefits aren’t immediately obvious and the costs of ignoring it don’t show up right away. But your health determines everything else: How hard you can work, how long you can pursue your goals, how much energy you have for your side hustle, and whether you will actually be around to enjoy the wealth you are building.

I’m not talking about spending thousands on expensive gym memberships or hiring personal trainers, although those might be worth it if you will actually use them. I’m talking about the basics that most people in their 20s completely ignore because they think they are invincible: Good food, regular sleep, and some form of exercise.

If you are constantly exhausted, stressed out, or dealing with health problems that could have been prevented, it doesn’t matter how smart your investment strategy is; you won’t have the energy or focus to execute it properly. The hidden cost of poor health in your 20s isn’t just medical bills, although those can definitely add up. It is the opportunity cost of not being able to work at full capacity, not being able to take advantage of opportunities when they arise, and potentially having to spend your later years dealing with preventable health issues instead of enjoying your wealth.

Plus, building wealth requires sustained effort over many years. If you’re running on fumes because you’ve been treating your body poorly, you are sabotaging your own success. The smart approach is to think of health investments as performance enhancers for everything else you are trying to accomplish.

Playing the Long Game: Connecting the Dots

Here is what ties all seven of these purchases together: They are all about playing the long game instead of optimizing for short-term gratification. Every single one requires you to think differently than most people your age. While everyone else is focused on looking successful right now, you are focused on actually becoming successful over time.

This is where the compound interest concept applies to more than just money. Every good decision you make in your 20s compounds into better outcomes later: Every side hustle skill you develop makes you more valuable in the marketplace. Every dollar you invest grows exponentially over decades. Every relationship you build can open doors years down the road. Every month you avoid car payments frees up capital for wealth-building activities.

The opposite is also true. Neglecting your health creates problems that get more expensive to fix over time. Credit card debt compounds against you. This is why your 20s matter so much. You are not just making decisions about today; you are making decisions about the trajectory of your entire life.

Prioritizing and Building Momentum

The mistake most people make is trying to do everything at once. They want to start three different side hustles, max out their retirement contributions, book trips to five countries, buy a house, and completely overhaul their diet—all in the same month. Then they get overwhelmed, abandon everything, and go back to buying stuff that makes them feel successful for about five minutes.

The smart approach is to prioritize these purchases based on your current situation and build momentum gradually. If you are drowning in high-interest debt, focus on generating extra income through a side hustle first. If you are already earning decent money but spending all of it, start with automating your index fund investments. If you are stable financially but stuck in your comfort zone, invest in education and travel to expand your perspective and opportunities.

Develop the Habits Today That Guarantee Success Tomorrow

Making smart purchases in your 20s requires you to be comfortable being different from your peer group. This is where the real test comes in: Can you handle your friends thinking you are “cheap” or boring? Can you resist the urge to upgrade your lifestyle every time you get a raise? Can you stick with your investment plan when the market drops?

The people who build wealth aren’t necessarily smarter or more disciplined than everyone else. They just developed better money habits earlier in life and let compound interest do the heavy lifting. The people who struggle financially often make the same fundamental mistakes over and over again because they never learn to think long-term.

These seven purchases are not just about building wealth. They are about building the kind of person who understands that real success is not about impressing strangers with stuff you cannot afford. It is about having the freedom to wake up every morning and decide what you want to do with your day, instead of what you have to do to pay bills. Start with one of these purchases today, because 10 years from now, you will either thank yourself or wish you had.

💡 Frequently Asked Questions (FAQ)

Q1: What is the single best purchase a 20-something can make to secure their financial future?

A1: While all seven purchases are impactful, initiating automated contributions to low-cost index funds within a tax-advantaged account like a Roth IRA is often considered the most accessible and powerful wealth-building move. This harnesses the full power of compound interest over time with minimal ongoing effort.

Q2: Should I focus on investing my money or paying off debt first in my 20s?

A2: This depends heavily on the interest rate of your debt. High-interest debt (like credit cards) often compounds faster than potential investment returns, making it a critical obstacle to tackle first. Low-interest debt (like some student loans) might allow for a parallel strategy of aggressive repayment alongside initial long-term investments.

Q3: Is it better to invest in a side hustle or start investing in index funds first?

A3: Both are crucial. A successful side hustle can exponentially increase your income, providing more capital to invest in index funds. However, index funds are passive and reliable. A balanced approach is often ideal: prioritize establishing automated index fund contributions first, and use any surplus income or focus to invest in a side hustle that matches your skills.

Recommended Tags