our 40s are a fascinating pivot point. They are the defining decade, the bridge between the energetic experimentation of youth and the serious countdown toward retirement. When you hit 40, you’re often in your peak earning years, but you’re also often facing peak expenses—mortgages, childcare, aging parents, the whole bit. It’s easy to feel the squeeze.

But here is the absolute reality: your 40s are also the single most critical window to set the tone for the rest of your life. It’s no longer about simply accumulating wealth; it’s about strategic engineering. It’s about ensuring that by the time you reach 50, 55, or 60, you have options.

The goal isn’t just a big number in the bank. The goal is choices.

You do not want to go into your 50s one paycheck away from a payday loan. You do not want to be 55 years old, looking at a personal financial hiccup and having to scramble like you were 25. By your 40s, you need your financial act together. You can see retirement on the horizon, and you need to build a foundation that minimizes stress, panic, and uncertainty. If you execute correctly in your 40s, you can set yourself up for Financial Freedom, reduced stress, and even early retirement.

As someone who has spent significant time counseling clients through their retirement transitions, I know that the decisions you make between age 40 and 49 radiate outward for the next forty years. Living in California, I’ve seen firsthand how the high cost of living can amplify financial mistakes, making it even more important to have a precise blueprint during these peak years.

Here are the eight major financial milestones you absolutely must strive to accomplish in your 40s before you reach age 50.

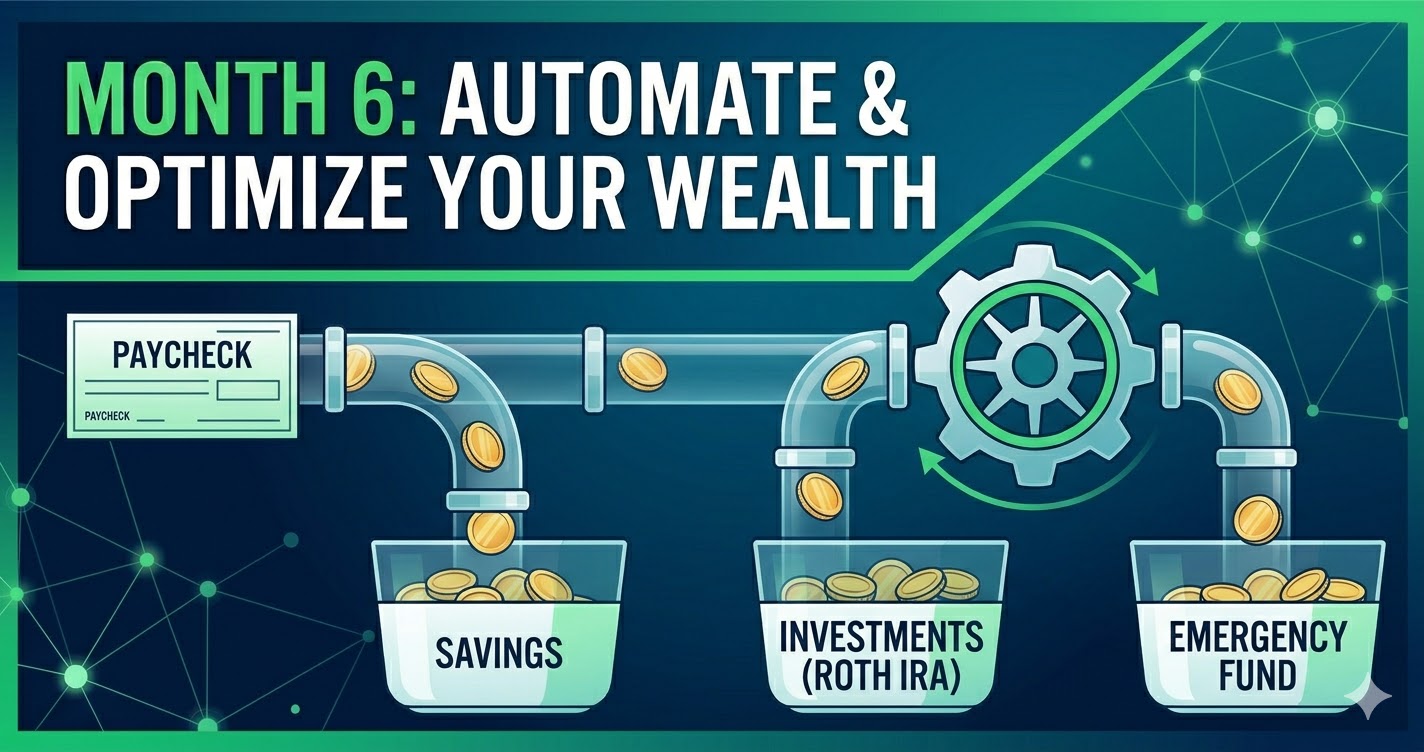

Milestone 1: Aggressively Maxing Out Your Retirement Investments

Your 40s are not the time to be cautious with your retirement contributions; they are the time to be relentless. This is the decade where the magic of compound interest still has enough time to explode, but your contribution power is at its peak.

If you are 40 years old, you likely still have another 15, 20, or even 25 years of working ahead of you. That is a massive asset—if you capitalize on it. You need to be lobbying as much money as possible into these vehicles.

Your goal should be to aggressively max out every available tax-advantaged retirement account:

- Your 401(k) or 403(b): In 2024, the contribution limit is $23,000 per year ($30,500 if you are 50 or older, but your goal in your 40s is to max that $23k). If your employer offers a match, failing to at least meet that match is a cardinal financial sin—it is guaranteed, 100% return on your investment that you are walking away from.

- Roth IRA or Traditional IRA: The current limit is $7,000 annually. A Roth IRA is particularly powerful in your 40s because it grows tax-free and allows for tax-free withdrawals in retirement.

If you find that you cannot max these out immediately, at the very least ensure you are contributing a significant and increasing amount. A good benchmark: by the end of your 40s, you should aim to have at least five to six times your annual salary saved in investments. If you’re at age 45 with $300k saved on a $60k salary, you’re on the right track. The closer retirement gets, the clearer the reality becomes that 55, 60, and 65 aren’t that far away.

Retirement Max-Out Checklist:

- Verify you are getting 100% of your employer’s 401(k) match.

- Set up automatic increases in your contribution rate (e.g., 1% more every year or with every raise).

- Evaluate your current total retirement savings against the 5x–6x salary benchmark.

- Understand catch-up contributions (which start at age 50) but strive to maximize base limits now.

Case Study: The 10-Year Delay

Consider two individuals, Susan and John. Susan begins maxing out her 401(k) ($23,000/year) at age 40 and continues until 60. Assuming a conservative 7% annual growth, her $460,000 in contributions would grow to approximately $1,114,000.

John waits until age 50 to begin maxing out his 401(k). Even if he makes catch-up contributions and contributes $30,500 every year from 50 to 60 ($305,000 total contributions), his portfolio would grow to roughly $477,000.

Despite the fact that John contributed a massive annual amount and utilized catch-up, Susan’s ten-year head start allowed compound interest to do the heavy lifting, resulting in over double the retirement nest egg. The lesson: Time is more powerful than timing.

Milestone 2: Achieving True Portfolio Diversification

When you were 25, you could afford to put all your money in a single, high-growth tech stock and weather the 50% drops. In your 40s, that is a recipe for disaster. While you are still investing for long-term growth, protecting what you have accumulated becomes equally important.

The second major milestone is ensuring strong diversification. This doesn’t mean just owning 10 different technology companies. It means owning different asset classes. You want to balance your overall portfolio:

- Individual Stocks: While rewarding, they carry highest specific risk.

- ETFs (Exchange Traded Funds) and Index Funds: These are essential. They provide broad market exposure (e.g., an S&P 500 or Total Stock Market index fund), giving you instant diversification across hundreds of companies.

- Real Estate: Either through physical property ownership or REITs (Real Estate Investment Trusts).

- Bonds: I am personally not the biggest fan of bonds for 40-year-olds because I believe they are too conservative, but having a small percentage (e.g., 10%) can reduce volatility.

Whatever you do, don’t get caught up in the trap of single-stock loyalty. You don’t want all your retirement hopes pinned on Nvidia, broadcom, or Amazon. The tech darlings of the 2020s might be the stagnant companies of the 2030s. The more you spread out your investments, the greater the protection for your money as it grows. Diversification isn’t about hitting home runs; it’s about ensuring your portfolio never crashes so hard that it can’t recover.

Milestone 3: Eradicating High-Interest (Bad) Debt

Debt on depreciating assets is a wealth-killer. Credit card balances, medical bills, and even some student loans are what we call “bad debt.” Why? Because you are paying interest to own things that are going down in value (or were already consumed). That interest is robbing you of the opportunity to put those same dollars toward growth.

The milestone here is straightforward: get this debt out of your way. Your 60-year-old self will look back and thank you immensely for becoming completely consumer debt-free at 45.

I cannot tell you how many people I encounter who are still working a job in their 60s simply and only because they have debt. They are chained to their paycheck because they are still paying off cars, student loans they took for their children, and credit cards. They missed the chance to be free decades earlier.

If you can eliminate this debt now, you free up massive extra cash flow that can be redirecting toward investing for your future. When you reach your 50s, you want to go in with momentum, not with payments dragging you down.

Bad Debt Payoff Strategies:

- The Avalanche Method (Mathematical): Pay minimums on everything, put all extra cash toward the debt with the highest interest rate first.

- The Snowball Method (Behavioral): Pay minimums on everything, put all extra cash toward the smallest balance first for quick psychological wins.

Whichever method you choose, commit to it in your 40s and vow never to go into debt for anything that depreciates in value again.

Milestone 4: Building a Rock-Solid, Fully Funded Emergency Fund

I mentioned this in the introduction, and it bears repeating: do not go into your 50s one paycheck away from a financial crisis. Life happens. Job losses, medical emergencies, major home repairs—they are not possibilities; they are eventualities.

The fourth major milestone is a fully funded emergency fund. This isn’t a savings account to buy a new couch; it’s an insurance policy for your financial life. Some people have this done in their 20s. Others struggle with it well into their 60s. Your 40s is the absolute deadline to secure this.

At a minimum, you must have 3 to 6 months of living expenses (or your essential needs—rent/mortgage, food, utilities, debt payments) sitting in a liquid, safe account (like a High-Yield Savings Account). If your monthly essential expenses are $5,000, your goal is $15,000 to $30,000.

You have been around enough to see how unexpected $1,000 or $1,500 emergencies derail lives. In your 40s, you must have the stability to handle these events without panic and without resorting to credit card debt or a payday loan.

High-Yield Savings Accounts (HYSAs) to Consider:

- As of early 2024, many HYSAs are offering rates of 4.50% APY or higher. Ensure any institution you use is FDIC insured.

Milestone 5: Cultivating Significant Home Equity

Milestone number five is for the homeowners. Your goal in your 40s is to build significant equity in your primary residence. When you have significant equity in a house, you have options.

If you are 38 when you take out a 30-year mortgage, that does not mean you are required to pay it off in 30 years. If you simply pay an extra couple of payments a year (or switch to bi-weekly payments), you can knock 10 or 11 years off that 30-year mortgage.

I know the common mathematical counter-argument: “I can make 7% in the stock market; why would I pay off a 4% mortgage early?” Mathematically, that makes sense. But human behavior and peace of mind are not always mathematical.

I have never, ever met a single person who paid off their home early and said, “You know what? That was a horrible idea. I wish I had that extra money in the stock market.” They just don’t say it. Why? Because they have absolute security. They own their roof.

Furthermore, if you are looking at retirement in your 50s or 60s, a paid-off home means your essential monthly living expenses plummet, meaning you need a smaller retirement portfolio to maintain your lifestyle. It’s a multi-layered financial win. You do not have to buy a home to be financially successful, but if you decide to, get significant equity working for you in your 40s.

Milestone 6: Creating Multiple Streams of Income

The sixth milestone is crucial for achieving true independence: developing diversified streams of income that are not reliant on your primary job. You don’t want your financial security dependent on a single company’s success or a single boss’s opinion.

When your primary income stops, whether by choice or by layoff, you face a terrifying gap. The goal in your 40s is to map out how you will fund your retirement when you are done working. You want to develop these streams now so they are mature by the time you retire.

Think beyond Social Security. At age 62, Social Security should be the icing on your financial cake, not the cake itself.

Possible Multiple Income Streams to Develop:

- Dividend Income: Investing in high-quality companies that pay a regular share of their profits to shareholders.

- Royalty Income: Income from creative work, intellectual property, or licensed assets.

- Rental Income: Acquiring rental properties (residential or commercial). This is excellent but requires management and initial capital.

- Business Profit: Starting or investing in a side business that can eventually operate without your daily involvement.

- Side Hustles: While these often start as active income, some can be scaled or structured into more passive avenues.

The goal is that by the time you decide you might not want to do what you are doing right now for work—perhaps when you enter your 50s—you already have other sources of income paying your bills.

Milestone 7: Solidifying Adequate Insurance on Everything

By the time you reach your 40s, you likely have more to lose than ever before. Yet, many people in this decade walk around with inadequate insurance. They may be single-income households with multiple dependents, or they may have significant assets but only basic liability coverage. This is a massive risk.

Your seventh major financial milestone is ensuring you have solid, comprehensive, and adequate insurance on all major components of your life:

- Health Insurance: This is non-negotiable. One major health crisis can wipe out a lifetime of saving.

- Life Insurance: Particularly critical if you have dependents. In your 40s, term life insurance is often very affordable and ensures that if the worst happens, your family can stay in their home and fund their goals. General rule: Aim for coverage that is 10x to 12x your annual salary.

- Disability Insurance: You are far more likely to become disabled during your working years than you are to die prematurely. If you can’t work, how do you pay the bills? Short-term and long-term disability insurance is crucial.

- Automobile Insurance: Ensure you have adequate liability coverage, especially given that in many states, basic requirements are far below the actual cost of significant accidents.

- Homeowners (or Renters) Insurance: Protecting your largest physical asset.

Ensure these policies are in place and reviewed annually in your 40s.

Milestone 8: Drafting and Reviewing a Comprehensive Estate Plan

The final major milestone is perhaps the most overlooked, yet it is arguably the most selfless one. You must take care of a comprehensive estate plan in your 40s.

An estate plan is not just about who gets your vintage car. It is a set of legal instructions that ensure that if something happens to you, your wishes are followed and your family (children, spouses, parents, nieces, nephews) is taken care of.

Without an estate plan, the state (not you) will direct exactly where all your stuff goes when you’re no longer here. If you are in the US, probate is a slow, expensive, and public process. An estate plan, often involving a will and a trust, can help your heirs avoid probate entirely.

Key Components of a 40s Estate Plan:

- A Will: Directing how your assets are distributed.

- A Living Trust: Which can hold assets and pass them directly to beneficiaries outside of probate.

- Financial Power of Attorney (POA): Designating who will handle your financial decisions if you become incapacitated.

- Healthcare Directive / Healthcare Power of Attorney: Explicitly stating your wishes for medical care and appointing someone to make those decisions if you cannot.

Having a solid estate plan established in your 40s is exactly like insurance. It ensures that what you have worked your life to accumulate goes to the people you want, exactly how you want. This $1,500 to $2,500 investment is often the single wisest money you will spend, minimizing bickering, fighting, and confusion for the people you love.

Estate Planning Checklist:

- Hire an estate planning attorney; avoid DIY online wills for complex family situations.

- Review all account beneficiaries (401k, life insurance, etc.) to ensure they match your estate plan.

- Store copies of your critical documents in a secure, accessible place and notify your designated POA and executors.

Conclusion: Act in Your 40s to Benefit Your 60s

There you have it: the eight major financial milestones to accomplish in your 40s. If you are reading this and you are in your 30s, fantastic—get it done now. Why wait? If you are already over 50 and reading this, that’s cool too; the best time to start was 10 years ago, but the second-best time is today.

Your 40s are the time to get these things in order because you start looking forward to what is next. You start realizing you won’t be here forever. Time moves exponentially faster as you age. The time between 30 and 40 seems like it went by in a flash. But let me guarantee you: 40 to 50 will come quicker than you think, and 50 to 60 even faster.

Let’s start preparing now. Share this information with someone in their 30s, 40s, or 50s who needs this reminder. And remember: the single absolute best person to take care of the “Old You” is the “Young You.”