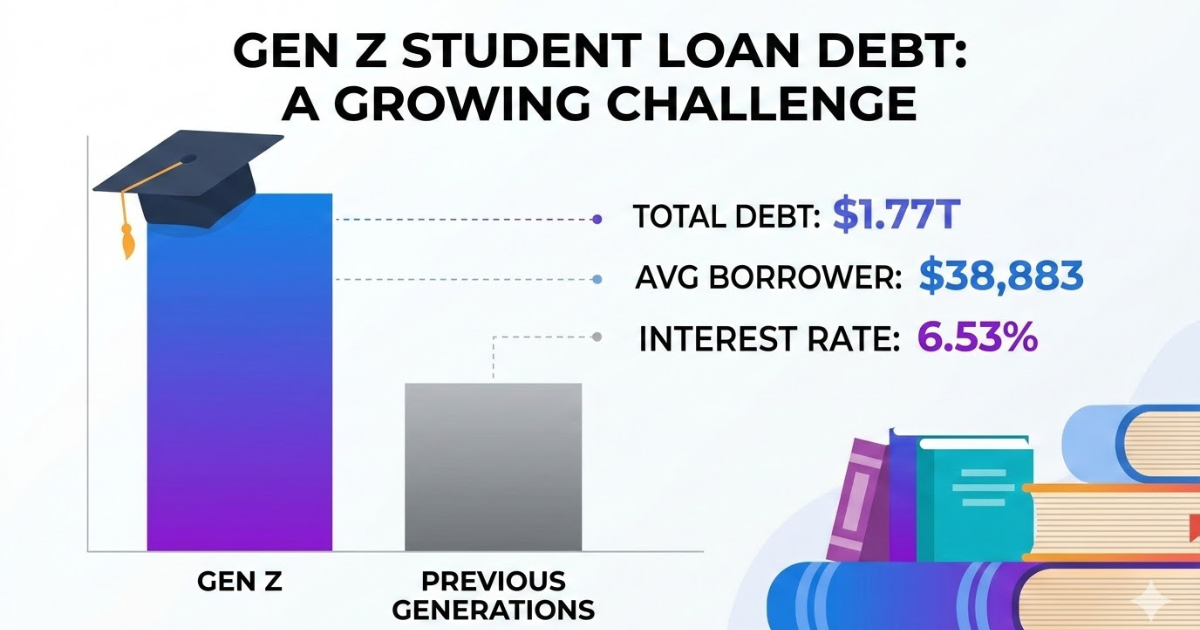

Navigating the landscape of personal finance today can feel like walking a tightrope between generations. On one hand, we have time-tested, analog methods championed by our grandparents. On the other, a surge of artificial intelligence and algorithmic tools promising to automate our way to financial freedom. Living here in Elk Grove, California, I’ve seen firsthand how the rising cost of living and shifting economic realities have forced people of all ages—from seasoned professionals to Gen Z—to get incredibly creative with their personal wealth management.

Whether you are trying to maximize your retirement contributions, manage a 1099-R distribution, or simply build a more robust emergency fund, understanding the psychology of saving is the first step toward lasting wealth. Recently, a fascinating blend of old-school tactics and new-age technology has taken center stage. Let us dive deep into the current wealth-building trends, evaluating the merits of the traditional envelope method, the rise of AI robo-advisors, and the viral savings challenges dominating social media.

The Timeless Power of the Envelope Method

Long before budgeting apps and automated spreadsheets existed, households relied on a physical, tangible way to manage their money: the envelope method. Also known today as “cash stuffing,” this strategy has experienced a massive resurgence, and for good reason. It works by attacking the fundamental psychology of how we spend.

The Psychology Behind the “Pain of Paying”

In our modern, cashless society, spending money has become entirely frictionless. You tap a piece of plastic, wave your smartphone over a terminal, or click “Buy Now” on a website. While incredibly convenient, this frictionless environment completely removes the psychological friction known as the “pain of paying.” When you swipe a card, your brain does not register a tangible loss.

The envelope method forces you to confront your spending reality. By withdrawing your budgeted discretionary income in physical cash and distributing it into categorically labeled envelopes (e.g., Groceries, Entertainment, Dining Out), you create a hard boundary. When you go to the store and physically hand over a twenty-dollar bill, you feel the transaction. More importantly, when an envelope is empty, the spending in that category stops. There is no overdraft, no credit card floating, and no borrowing from next month’s paycheck. You know exactly where every single dollar is going, which provides unparalleled mental tracking and budget enforcement.

How to Implement a Modern Cash Envelope System

If you find yourself constantly overspending in certain categories, implementing this method can be a highly effective reset for your financial habits. Here is a step-by-step guide to starting:

- Analyze Your Spending: Review your last three months of bank statements. Identify your “problem areas”—categories where you consistently exceed your intended budget, such as dining out or impulse shopping.

- Determine Your Cash Categories: You do not need an envelope for fixed expenses like rent, utilities, or auto loans. Reserve the envelopes strictly for variable, discretionary spending.

- Set Strict Limits: Assign a specific dollar amount to each category for the month or pay period.

- Fund Your Envelopes: Withdraw the exact amount of cash required and distribute it into your labeled envelopes.

- Commit to the Rule: Once the cash in the “Entertainment” envelope is gone, you cannot go to the movies until the next pay period. You must not borrow from the “Groceries” envelope to fund a night out.

The AI Revolution in Personal Finance

While the envelope method relies on manual discipline, the younger generations—particularly Gen Z and younger Millennials—are heavily leaning into artificial intelligence and automation to handle their money. If cash stuffing is about adding friction to your spending, AI-driven finance is about removing friction from your saving.

Spare Change Apps and Automated Micro-Investing

Prior to the full integration of AI, we saw the rise of micro-investing and automated savings apps. These tools operate on a simple premise: out of sight, out of mind. By linking your debit or credit card to an application, every purchase you make is rounded up to the nearest dollar. That “spare change” is automatically swept into a high-yield savings account or an investment portfolio.

For example, if you buy a coffee for $4.50, the app rounds the purchase up to $5.00 and transfers $0.50 into your savings. While fifty cents seems insignificant, these daily micro-transactions compound over weeks and months, effortlessly building a financial safety net for individuals who historically struggled to set aside large lump sums.

Robo-Advisors: Hands-Off Wealth Building

The introduction of advanced AI algorithms has taken automated savings a step further through the proliferation of robo-advisors. For years, investing in the stock market felt gatekept by high advisory fees and complex financial jargon. Many people wanted to build long-term wealth but were intimidated by the DIY (Do-It-Yourself) approach of picking individual stocks or balancing mutual funds.

Robo-advisors bridge this gap beautifully. When you sign up, the AI guides you through a detailed questionnaire assessing your age, income, financial goals, and, most importantly, your risk tolerance. Based on your inputs, the algorithm constructs a highly diversified portfolio—typically comprised of low-cost Exchange Traded Funds (ETFs).

Why AI Wealth Management Works:

- Emotionless Investing: The AI does not panic during market downturns. It systematically rebalances your portfolio according to your original target allocation, buying low and selling high automatically.

- Tax-Loss Harvesting: Advanced robo-advisors use algorithms to sell securities at a loss to offset capital gains tax liabilities, a complex strategy that was once exclusively available to high-net-worth individuals using human wealth managers.

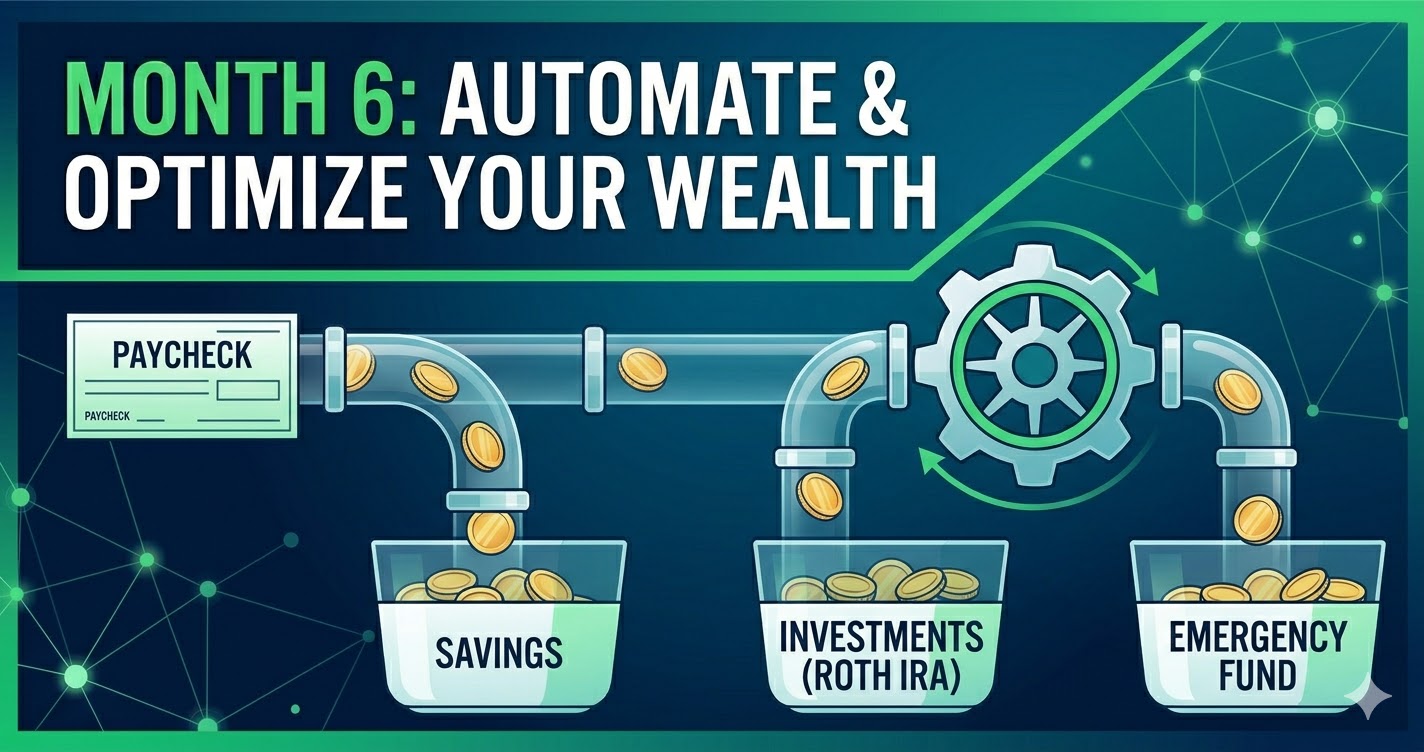

- Automated Contributions: You can set the AI to automatically pull a set amount from your paycheck before you even see the dollars in your checking account. This “pay yourself first” methodology is the bedrock of building smart wealth.

Viral Wealth: Evaluating Social Media Savings Challenges

If you spend any time on social media platforms like TikTok or Instagram, you have likely encountered viral savings challenges. From the “No-Spend Month” to the “100-Envelope Challenge,” these trends are heavily influencing how younger demographics interact with their finances. But do they actually work in practice?

The Gamification of Saving

The short answer is: yes, they can work, but typically only in the short term. The primary reason these challenges gain so much traction is that they gamify the act of saving. Personal finance can often feel dry, restrictive, and tedious. By turning it into a challenge with a clear beginning, middle, and end, savers get a dopamine hit every time they check off a box or stuff another envelope.

Take the popular “100-Envelope Challenge,” for instance. You number 100 envelopes from 1 to 100. Over 100 days, you draw an envelope at random and put the corresponding dollar amount inside. By the end of the challenge, you have saved exactly $5,050. It provides a highly visual, interactive way to achieve a significant financial milestone.

The Pitfall: Forgetting Your “Why”

However, there is a critical vulnerability in relying solely on viral challenges: the lack of a foundational purpose. Financial experts often note that participants in these challenges are highly motivated by the novelty of the trend (“Hey, look what I did!”), but once the challenge ends, they quickly revert to their old spending habits.

Saving money for the sheer sake of completing a social media trend is not a sustainable wealth-building strategy. To create lasting financial stability, there must be a profound, personal goal behind the behavior. You need a “why.” Are you saving to maximize your IRA contributions? Are you preparing for a tax hit on a recent 1099-R distribution? Are you building a down payment for a house, or aiming for early retirement?

Without a goal, the money saved during a challenge often ends up being frivolously spent as a “reward” for finishing the challenge, entirely defeating the purpose of the exercise.

Building a Hybrid Savings Strategy for Long-Term Wealth

The most successful wealth builders do not lock themselves into just one methodology. Instead, they synthesize these trends into a comprehensive, hybrid strategy tailored to their unique behavioral tendencies.

Step 1: Automate the Foundation

Start by leveraging technology. Set up a robo-advisor or an automated transfer with your primary bank. Ensure that a percentage of every paycheck (ideally 15% to 20%) is immediately routed into your retirement accounts and emergency savings before you have a chance to spend it. This handles your long-term “why” without requiring daily willpower.

Step 2: Control the Variables with Cash

If you still find your discretionary spending creeping up, apply the envelope method specifically to your trouble areas. Let the AI handle your wealth building, but use physical cash to manage your weekly grocery or entertainment budgets to reinstate that crucial “pain of paying.”

Step 3: Use Challenges for Short-Term Boosts

Reserve viral savings challenges for specific, short-term goals. If you want to fund a summer vacation or buy a new laptop without dipping into your core savings, initiate a 30-day no-spend challenge or a mini envelope challenge. This provides the gamified motivation you need without distracting from your overarching financial plan.

Ultimately, whether you are relying on the tangible friction of cold, hard cash, or trusting an algorithm to optimize your asset allocation, the core principle remains the same: intentionality. By combining the psychological discipline of the past with the technological convenience of the future, you position yourself to build, protect, and enjoy smart, lasting wealth.