Living in California, I’ve seen firsthand how the skyrocketing housing market in places like Elk Grove and the broader Sacramento area has forced Gen Z to completely rewrite the financial playbook. If you are in your late teens or twenties today, you are facing a macroeconomic environment that is vastly different from the one your parents or grandparents navigated. The traditional blueprint—go to an expensive college, buy a starter home at 23, and work the same corporate job for forty years—is no longer a guaranteed path to prosperity. In fact, following that outdated advice might just lead you straight into a financial trap.

However, despite the pessimistic headlines, Gen Z possesses unprecedented advantages. From the democratization of financial education to the explosion of the gig economy, young adults today have the tools to build sustainable, long-term wealth faster than any previous generation. This comprehensive guide will break down the exact hurdles Gen Z faces, the unique perks they can leverage, and the actionable strategies required to achieve true financial independence.

The Reality Check: Why Gen Z Has It Harder

Before we can strategize for the future, we must acknowledge the very real economic headwinds that young adults are facing today. It is not just about skipping the avocado toast; the fundamental math of living expenses has shifted dramatically.

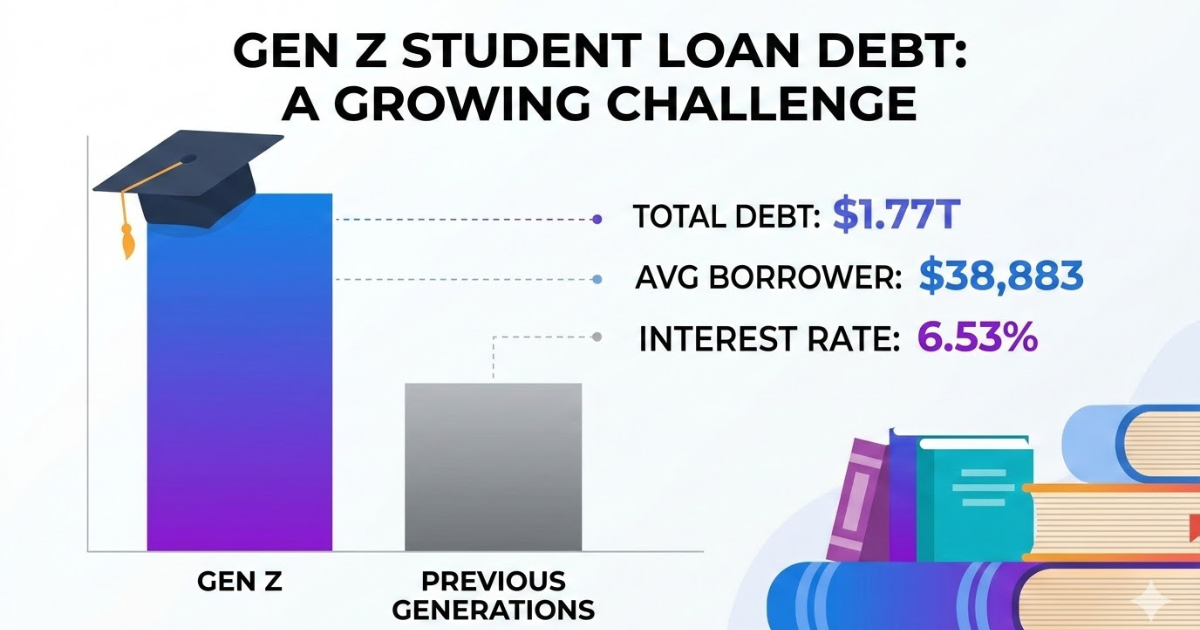

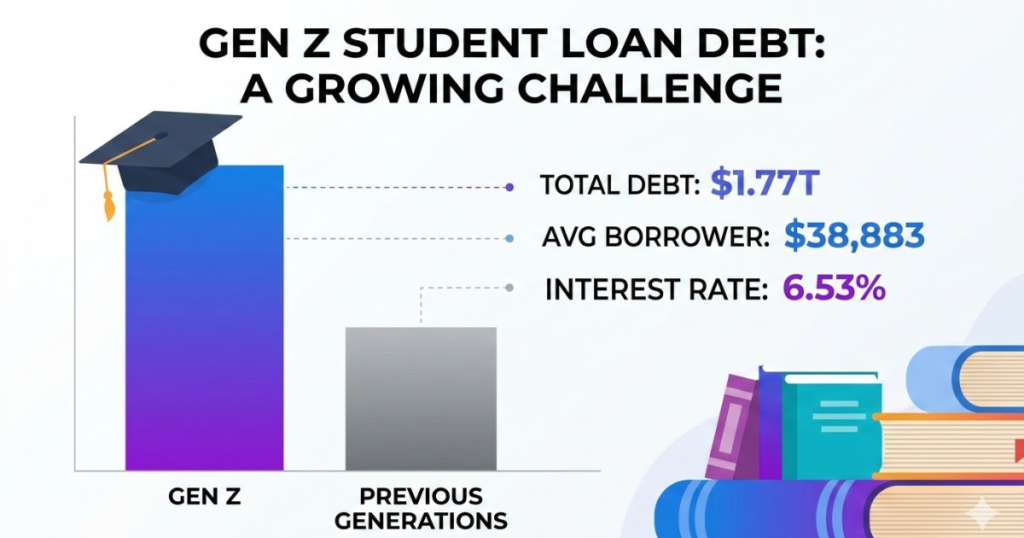

The $1.77 Trillion Student Loan Crisis

The most significant anchor tying down the financial potential of young adults is the student loan crisis. The total amount of student loan debt in America sits at a staggering $1.77 trillion. The average borrower graduates with $38,883 in debt, carrying an average interest rate of 6.53%, resulting in a monthly payment of over $200 before they even secure their first entry-level job.

The narrative pushed by society, guidance counselors, and well-meaning parents over the last two decades was to “go to the best school possible at all costs.” This has resulted in predatory lending practices and a generation starting their adult lives heavily in the red.

Expert Tip on Higher Education: If you have not yet taken out student loans, do everything in your power to avoid them. Consider in-state community colleges, trade schools, or taking a gap year to work and save. A degree from a prestigious, expensive university is rarely worth the crippling debt that follows, especially if the corresponding salary does not justify the ROI (Return on Investment).

The Real Estate Trap and High Inflation

The dream of homeownership has become incredibly daunting. In 2023, mortgage interest rates reached a 20-year high, and inflation peaked aggressively before settling around 2.5% in late 2024. These compounding factors mean that both the cost of borrowing money and the cost of everyday goods have surged simultaneously.

Furthermore, social media has skewed expectations. Platforms like Instagram and HGTV have conditioned many young buyers to expect a fully renovated, aesthetically perfect “forever home” as their first purchase.

The Golden Rule of Real Estate: The math of wise homeownership has not changed, even if the market has. When you are ready to buy, aim for a 15-year fixed-rate mortgage where the monthly payment is no more than 25% of your take-home pay. You may need to compromise on location or aesthetics, or save for a longer period to secure a 5% to 20% down payment, but adhering to this formula ensures you own the home, rather than the home owning you.

Convenience Culture and Subscription Fatigue

Gen Z grew up in an era where unprecedented convenience is just a screen tap away. Ride-share apps, instant food delivery, and endless streaming subscriptions are heavily ingrained in daily life. However, this convenience comes at a premium.

What feels like a series of small, harmless micro-transactions—$15 for a quick delivery, $12 for a streaming service, $20 for an aesthetic brunch latte—quickly snowballs into hundreds of dollars hemorrhaged each month. This “death by a thousand cuts” makes it incredibly difficult to save for substantial wealth-building assets like real estate or retirement funds.

Gen Z’s Unfair Financial Advantages

While the economic landscape is tough, Gen Z is equipped with tools that Millennials and Baby Boomers could only dream of. By leveraging these assets, young adults can bypass traditional gatekeepers and accelerate their wealth accumulation.

Free Financial Education at Your Fingertips

You no longer need a finance degree to understand the stock market, tax strategies, or real estate investing. We are living in the golden age of information. High-quality, actionable financial education is available for free via YouTube, specialized podcasts, and AI tools like ChatGPT.

Young adults are waking up to the power of compound interest much earlier. It is no longer uncommon to see teenagers taking an active interest in index funds or Roth IRAs. Because time is the most critical variable in compound interest, a 19-year-old who starts investing $200 a month will easily outpace a 35-year-old investing $600 a month by the time they both reach retirement age.

The Gig Economy and Boundless Career Options

The days of relying solely on a single 9-to-5 income are over. The modern economy offers endless avenues to generate active and passive income.

- Digital Real Estate: Managing social media for local businesses, starting a niche blog, or creating digital products on Etsy.

- Service-Based Hustles: Dog sitting through apps, driving for ride-share or grocery delivery services on weekends, or freelance video editing.

- The Circular Economy: Flipping items on Facebook Marketplace, selling vintage clothing on ThredUp, or refurbishing furniture.

If a traditional college path doesn’t make financial sense, the market now heavily rewards specialized skills. Trade schools, coding bootcamps, real estate licenses, and cosmetology certifications often provide a faster, debt-free route to a six-figure income than a standard four-year university degree.

Data Privacy as Wealth Protection

Growing up digitally native means your personal data is scattered across the internet, making you highly susceptible to data brokers, phishing scams, and identity theft. Protecting your identity is a modern pillar of wealth protection. Utilizing services that actively remove your personal information from public databases is no longer a luxury; it is a necessity to ensure your financial accounts and credit score remain uncompromised.

Case Study: The Power of Intentional Choices

Let’s look at a hypothetical scenario to illustrate the difference between following the “standard path” and utilizing a modern wealth-building strategy.

The Standard Path (The Debt Trap):

- Action: Attends an out-of-state private university for the “experience.”

- Result: Graduates with $85,000 in student loans. Secures a job paying $55,000/year.

- Lifestyle: Rents a luxury apartment to maintain an aesthetic social media presence, uses food delivery apps daily, and carries $8,000 in credit card debt.

- Net Worth at 25: -$90,000.

The Gen Z Wealth Strategy (The Intentional Path):

- Action: Attends a local community college for two years, then transfers to an in-state public university. Works a side hustle (freelance social media management) during school.

- Result: Graduates entirely debt-free. Secures a job paying $55,000/year, but maintains the side hustle bringing in an extra $15,000/year.

- Lifestyle: Rents a modest apartment with a roommate. Uses a zero-based budget. Automates $1,000 a month into a Roth IRA and S&P 500 index funds.

- Net Worth at 25: +$65,000.

The difference in these two scenarios isn’t luck or family inheritance; it is the intentional avoidance of debt and the rejection of convenience culture.

Expert Wealth-Building Habits to Adopt Today

If you want to change your family tree and build generational wealth, you must automate healthy financial habits and introduce friction to your bad ones.

1. Implement a Zero-Based Budget

The most critical habit for wealth building is telling your money where to go instead of wondering where it went. A zero-based budget means your income minus your expenses equals zero. Every single dollar is assigned a job—whether that job is paying rent, funding your retirement, or buying a coffee.

Using budgeting apps removes the mental fatigue of tracking expenses manually. It provides guilt-free permission to spend within your established boundaries while ensuring your saving goals are aggressively met.

2. Practice Contentment Over Aesthetics

A major wealth-killer for young adults is the pressure to curate a perfect life online. Going into debt to fund a vacation for Instagram photos, or financing a car you cannot afford to impress strangers, will keep you broke. True wealth is often quiet. Learn to be content with what you have, seek out low-cost experiences, and prioritize your actual bank account over your digital facade.

3. Choose Your Life Partner Wisely

From a purely financial perspective, who you marry is the single most important wealth-building decision you will ever make. If you and your spouse are aligned on financial principles, communicate openly about budgets, and share the same long-term vision, you will build wealth exponentially faster than someone who is constantly battling a partner over hidden debt or reckless spending.

The Gen Z Financial Independence Checklist

Ready to take control? Follow this step-by-step checklist to pivot from financial survival to aggressive wealth accumulation.

- Step 1: Audit Your Subscriptions. Cancel everything you haven’t used in the last 14 days. If you truly miss it, you can resubscribe next month.

- Step 2: Establish a Starter Emergency Fund. Save $1,000 immediately in a High-Yield Savings Account (HYSA) to act as a buffer between you and life’s minor emergencies.

- Step 3: Eliminate Consumer Debt. Use the Debt Snowball method to aggressively pay off credit cards, personal loans, and auto loans.

- Step 4: Gamify Your Income. Challenge yourself to make an extra $500 this month outside of your primary job. Sell old clothes, do freelance work, or pick up a weekend shift.

- Step 5: Automate Your Investments. Set up an automatic transfer from your checking account to your brokerage account or Roth IRA the day after your paycheck hits. Pay your future self before you have the chance to spend the money.

- Step 6: Plan Your Housing Strategy Conservatively. If you are planning to buy, ensure you are completely debt-free, have a 3-6 month emergency fund, and have saved a minimum of a 5% down payment.

Gen Z has the tenacity, the technological fluency, and the skepticism of broken traditional systems required to build incredible wealth. By rejecting the normalization of debt and harnessing the power of the modern digital economy, you can absolutely achieve financial freedom. The tools are all right in front of you—now it’s time to get to work.

🌿 Weekly wellness, health & beauty insights — straight to your inbox

Free subscription · Cancel anytime