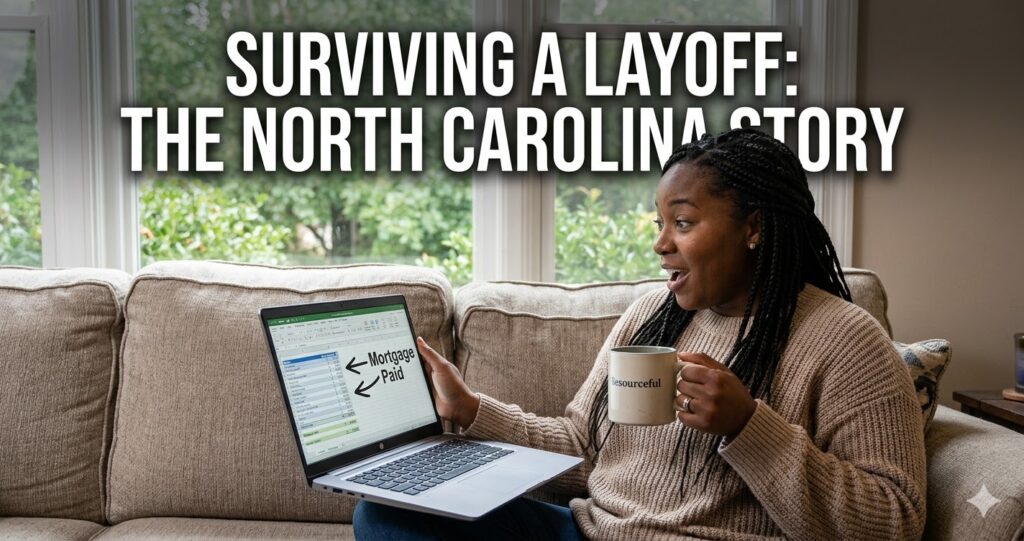

When the layoff email hit my inbox in January, the room went cold. It started like a regular Tuesday in my North Carolina home—the home I had purchased less than a year prior. The subject line was vague: “Clear your calendar, we need to meet in an hour.” I had that immediate, sinking gut feeling. I was a UX Content Designer making a comfortable $131,000 salary at a retail digital company. Within an hour, I was jobless, panicked, and very, very scared.

Ten months into this journey, however, my brain has been completely rewired around money.

Every single month since that day, I have successfully covered my $2,746 mortgage without a full-time job. Living in California, I’ve seen my friends panic over sudden rent hikes, but owning a home and losing your primary income is a unique kind of pressure. Yet, I haven’t made a single late payment. If you are facing a layoff or fear one, this isn’t just about making ends meet; it’s about becoming resourceful, taking decisive action, and redefining what professional stability looks like in America today.

Here is the exact blueprint I used to navigate sudden unemployment while maintaining my home.

The Day of the Layoff: Why I Recorded It (and Why It Went Viral)

The immediate wave of emotion was overwhelming: scared, nervous, anxious. I cried. But I didn’t just cry; I made the strange decision to document it. I recorded the moment I was laid off and the raw, vulnerable feelings that followed. I said, “I don’t know what’s gonna happen.”

Within a week, that video on my long-standing personal finance YouTube channel had exploded to 500,000 views—a viral moment I never saw coming. It was a massive silver lining in a dark cloud. That viral video, and the realization of the potential income it could generate, redefined my entire year. It gave me the first glimmer of hope and a scalable, new goal: content creation as my primary business.

A Sub to the channel is the best way to hold on to future content.

Mapping Your Income Strategy Post-Job

You cannot just rely on hope when your biggest bill is $2,746. Once the shock fades, you must systematically look for every available financial lever in the US system. I used a combination of traditional benefits and aggressive diversification to stay afloat.

Step 1: Secure Government and Company Benefits

I applied for unemployment benefits the week I was laid off. In North Carolina, the process can be slow, but it provided exactly $600 per week for 12 weeks. While $7,200 total doesn’t cover my mortgage (it’s less than three months’ payment), it covered my student loans, food, and health insurance. Company-wise, I received my last paycheck (two weeks), unused PTO, a small severance, and, in the spring, last year’s bonus. These were crucial in my first three months.

Step 2: The $21,000 Diversified Hustle Blueprint

This is where true survival happens: replacing your job with a diversified income stack. This year, through YouTube alone, I made around $21,000. My income on the platform fluctuates, peaking at $5,900 a month but dipping to $900. To achieve consistency, I treat it like a 9-to-5.

My strategy involves three long-form videos a week (posted on Mondays, Wednesdays, and Fridays) with shorts sprinkled in between. The revenue breaks down into key categories visualized below:

As you can see, I don’t rely on just one source. My total $2,000 avg./mo. comes from:

- Ad Revenue: (The largest piece of the pie) From my personal finance videos, particularly the viral layoff content.

- Sponsorships & Brand Deals: Companies paying to be featured on my channel.

- Digital Products: Templates I built from my own needs. I sell a budgeting template and a job search tracker through my YouTube channel, averaging another stream of income.

- Physical Products: T-shirts, sweatshirts, and other clothing items for my audience.

- VA Work: I work as a virtual assistant for a Pilates studio. This adds a consistent $300 per month in administrative assistant income.

The Cutting Edge: Restructuring My Expenses

I spent hours mapping out every single US bill. My annual UX content designer salary of $131,000 meant I was able to manage my $2,746 mortgage on an 1100–1200 square-foot North Carolina house that I bought for right under $340,000 with a $14,000 down payment/closing cost.

Once my income dropped from $131k to a variable $24k total, I had no choice but to slash expenses.

By far, my biggest bill is my mortgage. Everything else had to be scrutinized. Outside of the mortgage, I now have to pay for:

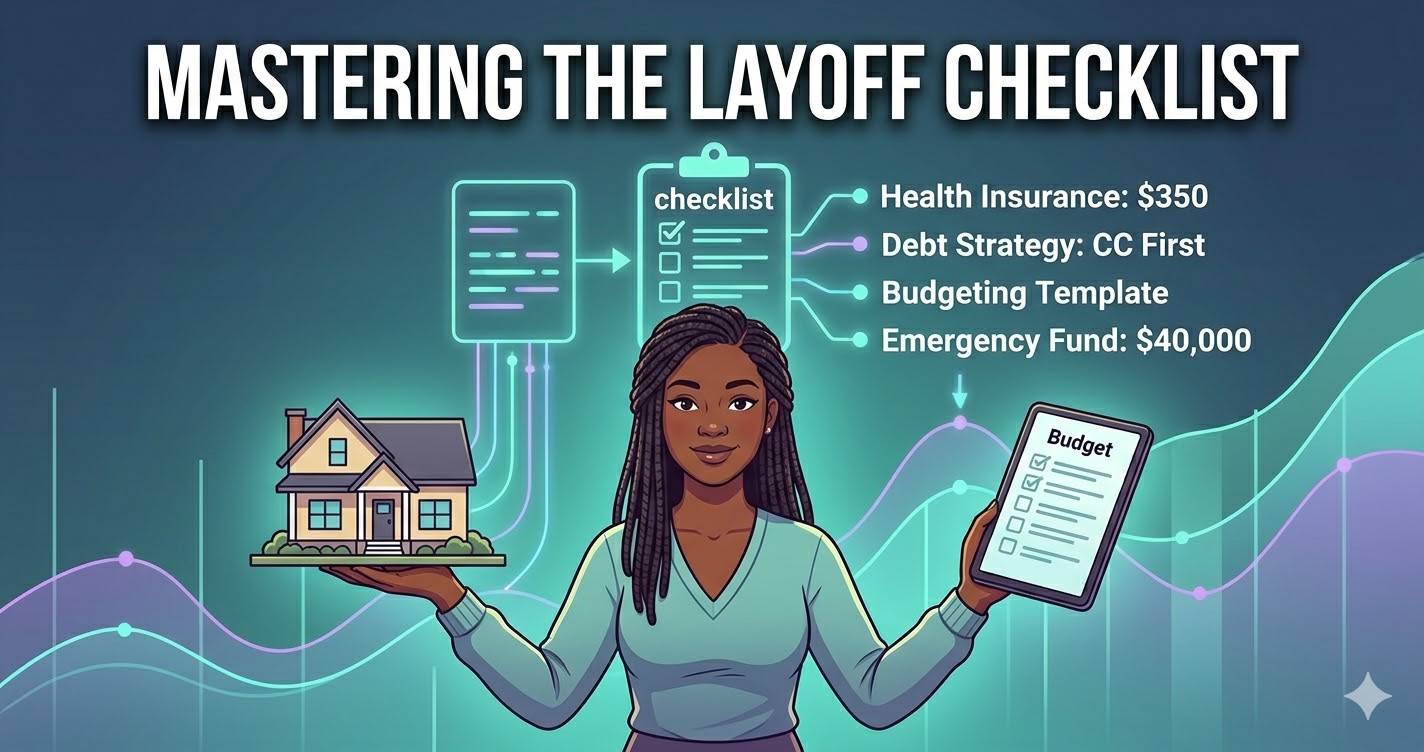

- Health Insurance: This new expense is $350 per month.

- Student Loans: Totaling $33,000 from my master’s degree, these require a **$223** monthly payment.

- Credit Card Debt: I am paying $200 per month for credit card debt.

- Other Slashing: I cut close to $1,000 in other, smaller monthly expenses, starting with how I shop. I only buy something when I need it, and I changed where I shop to prioritize necessities.

My plan is focused on aggressive debt repayment now. I immediately want to pay off the credit card debt, and then I would want to move into the student loans.

The 4-Part Layoff Survival Checklist

Facing a layoff while managing a mortgage in the United States requires precise, logical action. You cannot afford to let panic make decisions for you. This is the checklist that saved my home and my sanity.

Here is the exact action plan derived from my experience (and the numbers I use to manage my life):

- Prioritize the Primary Debt: In my case, it’s the $2,746 mortgage. I bought my home in spring 2024 for just under $340k, with $14k in closing/down payment. Everything else I have to make must cover this first.

- Stack the Side Hustle Income: My diversified $2k/mo. comes from ad rev, VA work, and digital templates like the budgeting one visualized. I use these funds to cover the $350 health insurance and the $223 student loans.

- Debt Strategy: Don’t just make a payment. I prioritize the highest interest rate first, starting with my credit card debt ($200/mo.) before tackling my $33,000 student loans.

- Use the Emergency Fund Correctively: While my $40k fund exists, I haven’t used it for most of this year. It wasn’t until I hit the 10-month mark that I finally had to pull money out of it. This fund is not for paying bills; it is for surviving the gaps between income streams.

A Sub to the channel is the best way to hold on to future content.

Job Searching vs. Business Building: The Hard Truth

Facing this difficult decision to restructure, you might be tempted to just focus on a full-time job. But as Symone Austin’s story shows, the job market right now is very, very tough.

My initial annual UX salary was $131,000. Now that I’m like ten months into this journey, I would say that I am open to a lot of different um jobs. I am still interested in UX design or content design, but I am also actively applying to social media-type jobs as well.

This toughness in the market is precisely why you cannot wait. You must treat your side hustle like your job. Tuesdays and Thursdays I focus on getting a full-time job again. Mondays, Wednesdays, and Fridays I focus on content creation. Without that discipline, I would not be paying my bills.

The Mental Health Crisis: How I Kept Going

A year after the layoff, I can tell you that my brain has been rewired. Moving my body is non-negotiable for my mental health. I still go to the gym, making sure that I’m going for walks when I can.

Mentorally, just doing things where I can turn off my brain for a second and just focus on something else helps. I read on my Kindle through the Libby app or do digital coloring on my iPad, things like that. These physical and mental actions aren’t “indulgences” during unemployment; they are essential systems to avoid a mental breakdown when your entire financial foundation is shaking.

FIRE Goals: Looking Forward, Not Back

Living in North Carolina and facing a layoff has changed my perspective. Long-term, I still want to pay off the credit card debt. In an ideal world, I’d like to pay off the student loans.

I’m interested in one day being a part of the FIRE (Financial Independence, Retire Early) community. The foundation I’m building now—the diversified income and extreme budgeting—is the groundwork for achieving that one day when I am financially stable again.

💡 FAQ

Q1: What were the most important initial steps Symone took within a week of her layoff to manage her US bills?

A1: Symone’s most vital initial steps were (1) immediately applying for unemployment benefits ($600/week) to stabilize her baseline cash flow, and (2) deciding to document and post her emotional reaction to the layoff on YouTube, which created a viral income opportunity and established her next professional pivot.

Q2: How did Symone Austin diversify her income stack to replace her $131,000 UX salary with consistent cash flow?

A2: She generated an average of $2,000 per month through a highly diversified strategy: (1) YouTube ad revenue and sponsorships from consistent content posting (3 times a week), (2) VA work providing $300/mo., (3) selling digital products (budgeting and job trackers), and (4) selling physical products (merchandise/clothing).

Q3: What specific strategies did Symone use to restructure her largest US monthly expenses during her unemployment?

A3: Her strategy involved (1) strictly adhering to a budgeting template (which she also sold as a digital product), (2) prioritizing her highest-interest debt by making a $200/mo. credit card payment before focusing on her $33k student loans ($223/mo.), (3) cutting **$1,000** in other monthly expenses, and (4) securing a roommate to start in January to significantly lower her $2,746 monthly mortgage payment.

🌿 Weekly wellness, health & beauty insights — straight to your inbox

Free subscription · Cancel anytime