Achieving financial freedom is often portrayed as a luxury reserved for those with massive salaries or inheritance. In fact, some of the most financially secure people I know don’t earn huge paychecks. Their secret isn’t a windfall; it’s a systematic blueprint for making their money work for them. As a qualified accountant and former investment banker, I have analyzed countless financial situations, and I can assure you that the same rules that build wealth on Wall Street apply on Main Street. Today, I’m sharing the exact blueprint that has helped thousands go from living paycheck to paycheck to building real, sustainable wealth. In the next 10 minutes, I’m going to show you how you can completely transform your financial life in just 6 months, by following this clear, month-by-month plan.

Month 1: Conquering the Ostrich Effect and Facing the Numbers

Defeating Psychological Avoidance

Living in California, where the cost of living feels like it’s constantly rising, I’ve seen many friends fall into the “Ostrich Effect” trap. The Ostrich Effect is a subtle but powerful psychological bias where people actively avoid unpleasant financial information. We convince ourselves that if we don’t check our bank account balance after a weekend splurge, or if we ignore a looming credit card statement, the problem somehow magically disappears.

The irony, of course, is that avoidance only magnifies the issue. Stress quietly mounts, small spending habits snowball into significant debt, and before you know it, you feel completely out of control. Month 1 is not about cutting back yet; it’s about bravery. It’s about ripping off the band-aid and taking full, unblinking control of your financial reality. The moment you face your finances head-on, clarity replaces anxiety.

Calculating Your ‘Core Four’

To gain that clarity, you need data, not guesswork. I recommend using a simple app or a dedicated spreadsheet—the specific tool matters less than its ease of use. If a tool feels like a chore, you won’t use it. Less friction is the key to creating a sustainable habit. This month, your only goal is to track your every penny to calculate your Core Four Numbers:

- Net Income: This is the precise amount deposited into your bank account after all taxes and deductions—your true take-home pay.

- Fundamental Expenses: The non-negotiables: rent or mortgage, utilities (electricity, water, internet), food (groceries only, not dining out), and critical transportation (fuel, insurance).

- Future You: This is any money that is already directed towards your future self, such as existing retirement contributions (e.g., a 401k) or automated savings transfers.

- Fun Spending: Everything else—dining out, entertainment, subscriptions, hobbies, and impulse buys. This is the category that usually surprises people the most.

You might feel uneasy as you gather this data. You may realize you are spending far more on subscription services or convenience food than you thought. But this knowledge is power. What we are doing in Month 1 is establishing the unbreakable foundation for the rest of your 6-month journey.

Month 2: Buying Your Freedom and Mastering Short-Term Sacrifice

The Short-Term Struggle for a Lifetime of Freedom

Once you have your Core Four numbers from Month 1, Month 2’s goal is dead simple: save one month’s worth of your fundamental expenses. Let’s say your fundamental costs are $2,500. That’s your target amount to have completely saved in a separate bank account by the end of the month.

I know what you’re thinking. “I can’t save my whole life’s expenses in a month.” But this one step alone moves you into the top percentile of people who actually take control of their money. Most people don’t get to this stage not because they can’t cut back, but because their brain fights against it.

Reframing Saving as Freedom

Humans are wired for immediate gratification, which makes saving feel like a loss or a deprivation. To succeed, you must radically reframe your relationship with money: You are not depriving yourself. You are buying freedom.

For the next 30 days, go all-in on that reframe. Cancel every single subscription service you barely use. Cook at home exclusively; no eating out. Postpone all non-essential purchases. It’s critical to remember that this “hit” is only temporary. If saving that amount in a single month feels too aggressive, you could spread it over two or three months, but be strictly honest with yourself. Don’t use a stretched-out timeline as an excuse to keep spending unnecessarily. The faster you build this foundational cushion, the sooner you break free from the stressful paycheck-to-paycheck cycle.

Month 3: Tackling High-Interest Debt and Establishing Your Safety Net

Separating Bad Debt from Good Debt

Many people spend years spinning their wheels by trying to simultaneously save and pay off debt. This often fails because they treat all debt as equal, not knowing what to target first. We need to categorize your debts strategically.

“Good debt,” like a mortgage or certain student loans, might have relatively low interest rates and is tied to an asset that could increase in value. “Bad debt”—credit cards, personal loans, or high-interest payday loans—is stopping you from moving forward and usually comes with incredibly high interest rates.

The Clear Debt Elimination Plan

Rank all your debt in terms of interest rate, from highest to lowest. Prioritize paying off every debt that carries an interest rate over 8% immediately, in that order. This is the absolute fastest way out of financial quicksand.

How much should you put toward this debt? Remember the Tracker data from Month 1? You already calculated what is left after paying for all your fundamental expenses. Take as much of that remaining “fun money” and funnel it directly into your highest-interest debt repayment plan.

Once you have cleared out all high-interest debt, shift your focus to securing your emergency fund. This strategy allows you to make much faster progress. Start by aiming for a starter emergency fund equal to 3 to 6 months of your fundamental expenses. If you have a stable job, start with 3 months. If your income is unpredictable, target 6 months.

But don’t get stuck here forever. A lot of people pause their financial growth to keep stacking cash. Month 3 is about security; Month 4 is about investing and wealth-building while you top up the remaining months.

Month 4: The Strategic Shift from Saving to Investing

Demystifying Investing: Start Sooner

A lot of people think investing is complicated, risky, or something you do only after saving for years. But the truth is, the sooner you start, the more wealth you’ll build. Let’s break it down into four straightforward steps.

Your Max Employer Match and Tax Benefits

First, maximize your employer’s retirement benefits. This is the easiest form of free money. If your employer offers a matching contribution, like a 401(k) match, contribute enough to get it. This is literally a 100% guaranteed return on your contributions. If you skip this, you’re not just saving; you’re leaving free money on the table.

Second, open a tax-advantaged investment account. Where you invest matters as much as what you invest in. If you’re in the UK, open up a Stocks & Shares ISA (a tax-free investment account). If you’re in the US, it’s e.g. a Roth IRA (a tax-free retirement savings account). These accounts let you keep more of your gains instead of losing them to tax.

Keep Investing and Wealth Building Simple

The third step is to invest in broad market funds. You do not need to pick individual stocks—in fact, most investment professionals cannot consistently beat the market. Instead, invest in low-cost index funds and ETFs. These vehicles automatically spread your risk across hundreds of thousands of companies. The S&P 500 alone has averaged a 10.5% annual return over the last 20 years—that’s the power of long-term investing.

And step four: keep building out your emergency fund without missing out on investing. You don’t have to choose between saving and investing; you can do both simultaneously. At first, you want to prioritize your emergency fund. Then, once you have established that foundational amount, you might want to shift to a 70% emergency fund and 30% investment allocation, then 50/50. And finally, once your emergency fund is fully topped up, you can focus 100% on wealth building. This way, you’re always moving forward, building security and growing wealth at the same time.

Month 5: Aggressively Increasing Your Cash Flow

Learning Opportunity vs. Earning Opportunity

Every job should give you one of two things: a learning opportunity or an earning opportunity. Ideally, you want both. But if you’re getting neither, you must take action. Either negotiate a pay raise or start exploring better-paying opportunities in your field. In most cases, switching jobs is the fastest way to increase your income, sometimes drastically. I’ve broken down my own salary year-by-year from my time in investment banking, and the biggest pay jumps always came when I moved. If you’re underpaid or undervalued, don’t wait for your employer to notice—make the move that benefits you.

The Power of Side Income Streams

If negotiating a salary or changing jobs feels daunting, or if you simply want to try something new, create a side income stream. Use the skills you already have to freelance, monetize a hobby, or build an online income stream from scratch. Even an extra $200 or $300 a month can massively speed up your savings and investments, accelerating your timeline to financial freedom. Month 5 is all about aggressively increasing the gap between your income and your expenses to maximize your surplus.

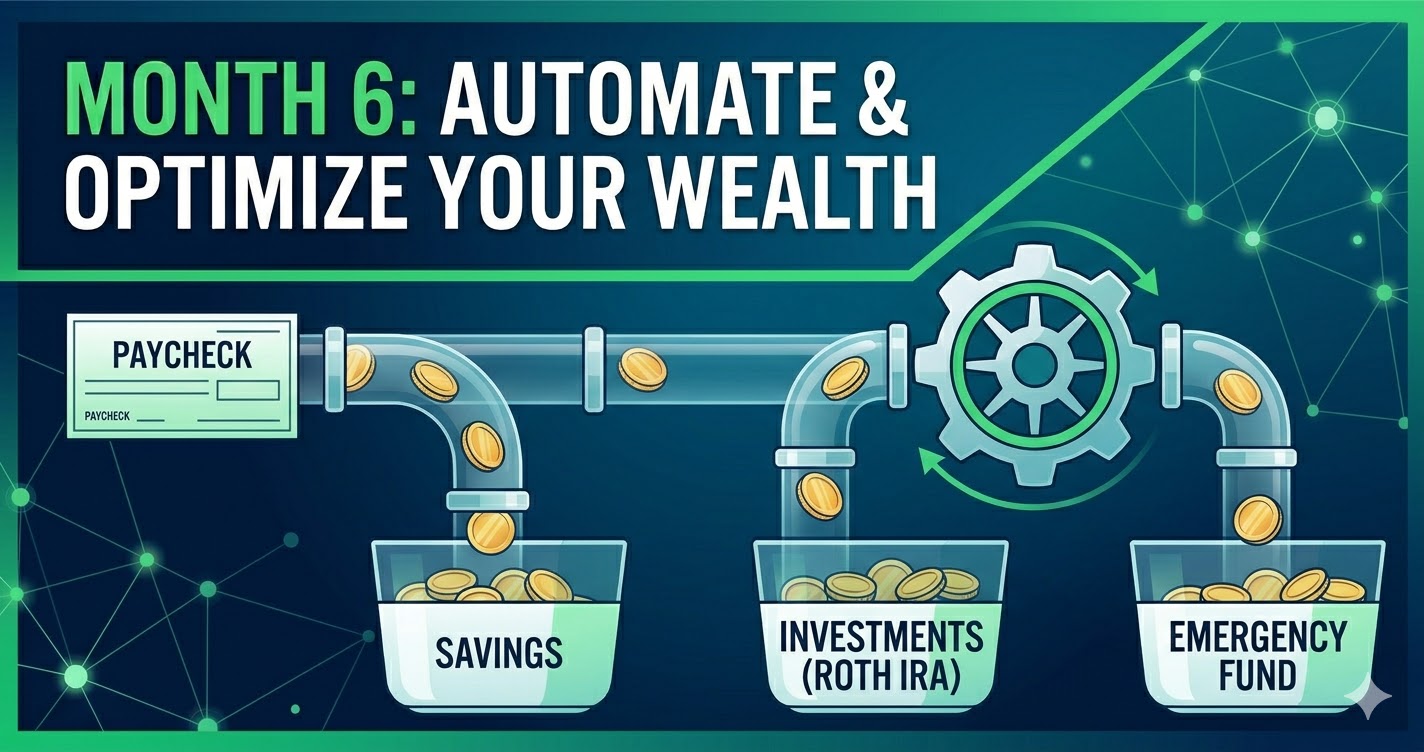

Month 6: Combatting Decision Fatigue and Optimizing for Long-Term Growth

The Psychology of Automation and Consistency

Have you ever heard of decision fatigue? It’s a real psychological phenomenon: the more choices we have to make in a single day, the worse our decisions become. By the time we get to the end of the day, our brains are exhausted, and so we default to whatever is easiest—whether that’s skipping the gym, ordering a takeout, or just ignoring our finances.

This is exactly why automation is one of the most powerful things you can do for your finances. When you rely on manual decisions to save, invest, or pay bills, you leave room for inconsistency. Some months, you’ll be on top of it; others, when life gets busy, you’ll fall behind. That’s why the secret to financial success isn’t self-discipline; it’s removing the need for discipline altogether.

Automating Your Money System and Ongoing Optimization

In this final month of the blueprint, we are doing two critical things. First, we are automating your entire money system: set up direct debits for rent, mortgage, utilities, insurance, and debt repayments. This prevents late fees and protects your credit score. Then, schedule automatic transfers to your savings, investment accounts, and retirement fund. You already know your numbers from Month 1, so you know what you can set up at this stage—and remember to pay yourself first, directing that money into your own pocket before paying anyone else. The remaining surplus is your everyday spending money, effortless to budget since you know exactly when it’s gone.

The second thing you want to do is review and adjust your financial plan. Your plan isn’t set in stone; your income changes, your expenses shift, and your goals evolve. Continue to educate yourself, checking in with yourself: “Are my automated savings and investments still aligned with my goals? Has my income increased? Can I increase my savings rate?” To stay up to date, you could always subscribe to this channel. I upload a new video almost every Sunday with the primary goal of helping you take control of your money and, ultimately, your entire financial life. Let’s finish this journey strong.