The True Cost of Living in the US in 2026: What to Expect

Every January, Americans tell themselves the same story: this will be the year things get easier. And every year, the grocery receipt, the rent notice, and the insurance renewal quietly disagree. Living in California, I’ve watched this pattern repeat for over a decade — but 2026 feels different. Not because the increases are dramatic in any single category, but because they are happening everywhere, all at once, and compounding on top of a household budget that has already been stretched thin since 2022.

This piece isn’t about panic. It’s about clarity. If you understand exactly where your money is going — and why — you can make sharper decisions before the next bill arrives. Let’s break down the real numbers behind the American cost of living in 2026.

Why 2026 Feels Different: The New American Budget Reality

Unlike the sharp inflation spike of 2022, 2026’s cost pressure is quieter but more persistent. Wage growth has slowed to roughly 3.1% year-over-year for most middle-income workers, while core living expenses — housing, food, insurance, and utilities — have continued climbing at a faster clip. The gap between what people earn and what they need to spend simply to maintain their existing lifestyle is widening, not narrowing.

The Numbers Behind the Headlines

- Median household income growth has trailed core expense growth for four consecutive years.

- Renters now spend an average of 32% of gross income on housing in major metro areas, above the traditional 30% affordability threshold.

- Grocery basket costs for a family of four have risen faster than the overall Consumer Price Index in six of the last eight quarters.

None of these numbers exist in isolation. A family that’s paying more for rent has less flexibility to absorb a spike in grocery prices. A family managing a higher insurance premium has less room to handle an unexpected car repair. This is the real story of 2026: not one crisis, but many small pressures stacking on top of each other.

Housing Costs Are Outpacing Wages

Rent vs. Mortgage: A 2026 Snapshot

Housing remains the single largest line item in nearly every American budget. In many mid-sized metro areas — think Columbus, Ohio or Raleigh, North Carolina — rents for a standard two-bedroom apartment have crossed the $1,700–$1,900 range, a level that would have been considered “coastal-city pricing” just five years ago.

Mortgage holders aren’t necessarily better off. With rates still elevated compared to the pre-2022 era, many homeowners who refinanced or purchased in the last two years are carrying monthly payments 40–60% higher than what a similar home would have cost in 2019.

Real Case Study: A Family in Ohio

Consider a hypothetical but realistic household: a family of four in suburban Ohio earning the regional median income of roughly $68,000 per year. After taxes, their take-home pay is approximately $4,650 per month. Their rent alone — $1,750 — now consumes nearly 38% of that income, well above the recommended threshold. This leaves less room for groceries, healthcare, transportation, and savings, forcing many families to make trade-offs that simply didn’t exist a decade ago.

Looking for practical ways to stretch your household budget? Browse curated home and lifestyle essentials that help American families save more in 2026.

Explore Budget-Friendly Picks on Amazon →Groceries: The Silent Budget Killer

How Grocery Inflation Actually Works

Grocery inflation rarely announces itself with a single dramatic price hike. Instead, it works through what economists call “shrinkflation” and “price creep” — a box of cereal that’s slightly smaller, a jar of peanut butter that’s a dollar more, a rotisserie chicken that’s suddenly $2 pricier than last month. Individually, these changes feel minor. Across a full monthly grocery run for a family of four, they add up to $150–$250 in additional spending compared to just two years ago.

Practical Tools That Cut Grocery Spending

One of the most effective — and often overlooked — ways households are fighting back against grocery inflation isn’t through couponing alone, but through smarter kitchen habits. Meal prepping, bulk cooking, and better food storage can meaningfully reduce both grocery bills and food waste. Here are five tools that consistently make a measurable difference:

- Meal Prep Containers — Portioning meals ahead of time is one of the simplest ways to stop impulse takeout orders, which often cost 3–4x more than a home-cooked equivalent. See the top-rated meal prep set on Amazon →

- Air Fryer — Beyond convenience, air fryers use significantly less energy than a full oven for everyday cooking, quietly trimming both grocery and utility costs. Check current air fryer deals →

- Multi-Cooker / Instant Pot — Batch-cooking proteins and grains in bulk lowers the per-meal cost dramatically compared to buying pre-made meals. View the best-selling multi-cooker →

- Vacuum Sealer — Food waste is an invisible tax on every household. Vacuum sealing extends shelf life for bulk-bought meat and produce, often paying for itself within a month. See the highest-rated vacuum sealer →

- Airtight Bulk Storage Containers — Buying pantry staples in bulk only saves money if the food stays fresh. Proper storage prevents spoilage-driven waste. Browse top storage container sets →

None of these tools is a silver bullet on its own. But combined, households that adopt even two or three of these habits typically report noticeable monthly savings — often in the range of $80 to $150 — without changing what they actually eat.

Healthcare: The Hidden Burden

Insurance Premiums in 2026

Employer-sponsored health insurance premiums have continued their steady climb, with many families now contributing $500–$700 per month toward coverage, even before accounting for deductibles. For households without employer coverage, marketplace plans can easily exceed $900 per month for a family of four, depending on the state and plan tier.

Out-of-Pocket Reality Check

Premiums are only part of the picture. High-deductible plans mean many families pay thousands out of pocket before insurance meaningfully kicks in. A single urgent care visit can cost $150–$300, and a routine specialist appointment often runs $200–$400 without insurance discounts applied. This is why preventive care — things like home blood pressure monitoring or basic first-aid preparedness — has quietly become a financial strategy as much as a health one; catching an issue early is almost always cheaper than treating it after an ER visit. For readers interested in a deeper dive into everyday wellness and preventive health strategies, our sister site WellbeingPrime covers this in more detail.

Managing rising costs takes the right tools. Take a look at practical, budget-friendly household essentials trusted by thousands of American families.

Shop the Full Collection →Transportation and Everyday Expenses

Gas, Cars, and Commuting Costs

Transportation remains the third-largest expense category for most American households, after housing and food. Gas prices have stabilized compared to their 2022 peak, but auto insurance premiums have risen sharply — often by 15–20% year-over-year in many states — driven by higher repair costs and more expensive vehicle technology. Combined with financing costs on new and used vehicles, many households now spend $700–$900 per month just to keep a car on the road, insured, and fueled.

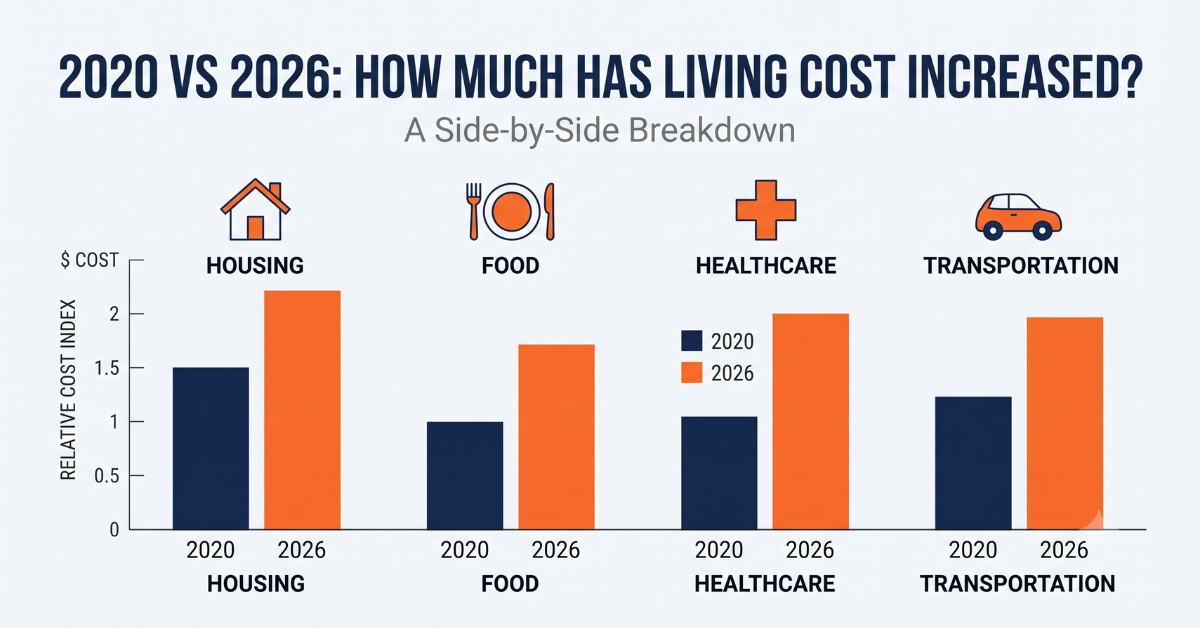

2020 vs 2026: The Full Comparison

Stepping back and looking at the six-year picture makes the shift clearer than any single statistic. Housing, groceries, healthcare, and transportation have all moved in the same direction — up — while wage growth has struggled to keep pace across nearly every income bracket except the very top. This isn’t a story of one bad year; it’s a structural shift in what it costs to simply maintain a stable, middle-class life in America.

How Americans Are Adapting

Smart Budgeting Strategies for 2026

The households weathering this environment most successfully aren’t necessarily earning more — they’re spending more intentionally. Some of the most effective strategies include:

- Auditing recurring subscriptions quarterly, not annually — small charges compound quickly when left unchecked.

- Batch cooking and meal prepping to reduce both grocery waste and impulse takeout spending.

- Reviewing insurance plans annually rather than auto-renewing, since premium creep often goes unnoticed for years.

- Building a small emergency buffer before optimizing for long-term savings, since unexpected expenses are often what derail an otherwise solid budget.

- Comparing energy and utility providers where deregulated markets allow it, since rates can vary significantly between providers in the same city.

If you’re navigating cost-of-living questions from an international or cross-cultural perspective — particularly comparing life in the US to South Korea — our companion site SeoulCast offers additional context on how these dynamics compare across countries.

Final Thoughts: Navigating the New Cost of Living

The true cost of living in the US in 2026 isn’t defined by one dramatic number — it’s defined by the cumulative weight of small, steady increases across nearly every category of household spending. Understanding exactly where that pressure is coming from is the first step toward managing it. Whether it’s rethinking how you shop for groceries, reviewing your insurance annually, or simply being more intentional about recurring expenses, the households that adapt fastest are the ones that come out ahead — not by earning dramatically more, but by spending with far greater clarity.

Recommended Tags

cost of living 2026, US inflation, household budgeting, grocery savings tips, personal finance America

💡 Frequently Asked Questions (FAQ)

Q1: Why does the US cost of living feel higher in 2026 even though inflation has officially slowed?

A1: Official inflation figures measure the rate of price increases, not the cumulative level. Even with a slower rate of increase, prices are still rising on top of an already elevated base from 2022–2024, which is why household budgets continue to feel tight.

Q2: Which single expense category has the biggest impact on a typical American family’s budget in 2026?

A2: Housing remains the largest single expense for most households, often consuming 30–38% of take-home income in mid-sized metro areas, followed by groceries and healthcare premiums.

Q3: Are there realistic ways to meaningfully lower grocery costs without changing what a family eats?

A3: Yes. Tools like meal prep containers, air fryers, multi-cookers, vacuum sealers, and airtight bulk storage help reduce food waste and cut down on costly takeout, often saving households $80–$150 per month without altering their actual diet.

🌿 Weekly wellness, health & beauty insights — straight to your inbox

Free subscription · Cancel anytime